Key Takeaways

- Despite growth valuations falling by twice as much as value in 2022, the relative value of value remains well above historic averages.

- Current valuation spreads are not much above average historic levels, further proof that fear of a recession is not yet priced into the markets.

- Opportunities arise during risk events as good stocks are thrown out with the bad, and we rely on our valuation discipline to find attractive stocks when no one wants them.

Still Early Stages in a Strong Value Cycle

In physics there is no absolute measure of time and space. Rather, as we know thanks to Einstein, everything is relative, with events having impacts on one another. Similarly, financial markets also don’t have an absolute measure of time and most things are indeed compared relative to each other. As a result, every market cycle is unique and the variability of time between events is one of the big challenges in investing. However, what we do know is that markets regularly cycle between hope and fear and, within this arc of human emotions, key events tend to repeat themselves under similar conditions. With relativity in mind, we think it is worth looking back at the big events of 2022 and what they suggest for the big opportunities in 2023.The first big change that we observed is that everything got cheaper as multiples were compressed. On an absolute basis, the multiple of the Russell 1000 Growth Index (RLG) compressed just over 30%, while the Russell 1000 Value Index (RLV) compressed almost 15%.

As with physics, however, what matters is the relative measure. Despite growth valuations falling by twice as much as value, the relative value of value remained well above historic averages and remained in the cheapest decile (Exhibit 1). The key observation here is that relative performance moves between growth and value styles have never stalled out at these levels. Market cycle arcs persist until completed, and there is still a long way to go in favor of value in this current market cycle.

Exhibit 1: Value Remains Historically Undervalued

As of December 31, 2022. Source: Bloomberg Finance, L.P., ClearBridge Analysis

Given how painful 2022 felt, particularly for growth investors, it may seem hard to believe that growth didn’t make more progress. To be clear, progress was indeed made, but what was worked off was only investor excess. Unfortunately, there is still a long way to go before fear is priced in.

We view market price movements as the function of valuation and fundamentals and, within valuation, seek to identify any changes in the risk-free rate (the 10-year Treasury yield) and the equity risk premium. Throughout 2022, nearly 100% of the change in the market’s valuation multiple was driven solely by the movement in interest rates, leaving the equity risk premium essentially flat. Another surprising observation from the year is that fundamentals were not a big drag on performance; RLV earnings grew 5% while RLG earnings grew 1%. In other words, the pain felt by investors was almost entirely the increase of the cost of capital as the Fed raised interest rates.

Exhibit 2: Capital Costs Driven by the Risk Free Rate

As of December 31, 2022. Source: Bloomberg Finance, Damodaran Online

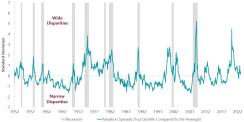

One of our key tactics as valuation-disciplined managers is monitoring valuation spreads and capitalizing on them when they get historically wide. Similar to high-yield spreads and volatility indices, valuation spreads typically explode higher during a recession. Current valuation spreads are not much above average historic levels (Exhibit 3), further proof that fear is not yet priced into the markets. While the value of value relative to growth still massively favors value as the big opportunity over the current market cycle, most U.S. stocks are not historically cheap and do not embed a recession on an absolute basis.

Exhibit 3: Valuation Spreads Near Historic Average

As of December 31, 2022. Source: National Bureau of Economic Research, Empirical Research Partners Analysis

Should the Fed indeed trigger a recession, valuation spreads will likely follow historic precedent and gap out. While the stocks unfortunate enough to drive spreads higher change with each occurrence, the list is typically comprised of the past cycle’s winners who have fallen from glory due to forced selling from excessive leverage or worsening fundamentals. Yesterday’s heroes become today’s villains as excesses are cut away. We think this will again be the case, with distress most concentrated in stocks that were the biggest beneficiaries of the free capital era and excessive speculation by investors armed with leverage and derivatives. However, the tactical opportunity to be gleaned comes as equity correlations skyrocket during risk events, and good stocks are thrown out with the bad. However, just because a stock is down 50% does not make it attractively cheap. To avoid anchoring expectations, we rely on our rigorous valuation discipline to help us navigate the carnage and find attractive stocks when seemingly no one wants them.