For active managers, emerging markets (EMs) may provide an opportunity to weather recent market volatility and potentially generate alpha. But emerging markets are not homogeneous. Pinpointing the reason for dispersion is critical to finding opportunities. Here are three areas of focus that can help achieve that goal in EMs.

Opportunity 1: Identify the winning sectors

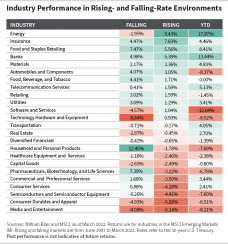

Industry performance has historically been affected by rising-rate environments. The strongest-performing industries in such environments over the past 25 years have been energy, insurance, consumer staples, banks, and materials.

“Right now, banks are appealing and an area of increased focus for us because they benefit from rising rates by earning more money on the loans they provide,” says Casey Preyss, CFA, partner, a portfolio manager for William Blair’s Emerging Markets Growth, Emerging Markets Small Cap Growth, China A-Shares Growth, China Growth, and Emerging Markets ex China Growth strategies.

Energy tends to perform well in rising-rate environments because the U.S. Federal Reserve typically raises rates when economic times are good. The knock-ons of that benefit energy stocks because consumers tend to make major investments.

It’s not easy to find quality growth companies in energy and materials, however, especially in EMs – but it can be done. “We’re focusing on countries in Latin America, the Middle East, and Indonesia that have the potential to benefit from higher commodity prices,” says Preyss.

The relative underperformers from a sector perspective are the highest-growth, highest-valuation segments of the market. Nothing is structurally broken in those industries, but they are growing into their valuations.

“When we plot corporate fundamentals as represented by our earnings trend model against valuations, the most attractive industries are energy, metals and mining, banks, and diversified financials,” says Preyss. “On the flipside, industries with more challenging fundamentals and expensive valuations are pharmaceuticals, healthcare equipment, retail, media, and software.”

In many emerging markets, sectors on the wrong side of regulation will have a much higher hurdle to overcome because of the threat to their business models. However, the opposite can also be true.

For example, the healthcare sector in key emerging markets has also long been appealing as an offshoot of consumption. As people get wealthier, they want better drugs, better medical devices, private hospitals, etc. As a result, investors valued the sector as one that offered high growth and high return on invested capital. But some countries have moved toward forced price reductions, resulting in plummeting valuations crashing down.

There are also external concerns affecting key sectors in emerging markets. For example, if the U.S. decides that a particular sector in a certain emerging market is a threat to national security and puts it on the “entity list,” stocks in this sector could be derated by investors.

“The other side of that coin is by focusing on companies in sectors that the government wants to be internationally competitive investors can uncover opportunities,” says,” says Todd McClone, CFA, partner, a portfolio manager for William Blair’s emerging markets strategies, including Emerging Markets Leaders, Emerging Markets Growth, Emerging Markets Small Cap Growth, and Emerging Markets ex China Growth. “Electric vehicle batteries and solar power supply chains are good examples.”

Opportunity 2: Countries with Easing Monetary Policy

Over the past decade, the economic performance and resulting earnings growth of emerging markets has disappointed relative to developed markets (particularly the U.S.).Since the global financial crisis, quantitative easing in developed markets has supported economic growth and equity market valuations. That policy option has not been readily available in emerging markets.

“This year, we believe much of the world will be tightening monetary policy,” says McClone. “The U.S. and Europe have already begun. Emerging markets, on the other hand, are coming out of the pandemic stronger, and growth is starting to pick up naturally.”

As an example, McClone points to Brazil and China, which last year were among the worst performing markets globally.

“In Brazil, valuations are already attractive in the wake of last year’s substantial derating, thanks to the Brazilian central bank aggressively raising interest rates in response to the spike in inflation. And investors are anticipating a peak in inflation and interest rates,” says McClone.

China, which was first out of the pandemic, has already begun easing monetary policy, albeit at a slower pace than the market hoped. However, “I believe the pace of easing should accelerate in the coming months and quarters, supporting economic growth, corporate profit growth, and equity market valuations which are currently at 10-year lows,” says McClone.

The dispersion in monetary policy cycles gives investors the opportunity to add exposure to countries where an easing monetary policy should support growth and valuations, and to avoid countries where the opposite is true. The point countries are at in their monetary policy cycles directly impacts the market’s perception of future economic growth and corporate profits, and, importantly, what multiples to pay for those profits.

Opportunity 3: Against the Grain in Russia-Ukraine

The conflict in Ukraine likely bodes poorly for Eastern Europe more broadly, expanding beyond Russia to Hungary, Poland, and other countries in the region.There are several reasons for this: eastern Europe is very dependent on energy imports from Russia; it is dealing with a refugee crisis from Ukraine; inflation has accelerated; currencies are under pressure; and interest rates have increased.

Perhaps most notably for investors, the conflict has boosted commodity prices, and, as a result, driven up inflation globally. Rising agricultural prices have pushed up food prices across emerging markets, where food is a much larger component of overall spending.

“We’ve seen how that plays out in the Middle East and Latin America, where food price increases have, in the past, caused economic and social disruptions,” says McClone. “However, rising agricultural prices have benefited emerging markets that are net exporters of these commodities.”

At the same time, the European embargo of Russian oil and gas also has winners and losers. Russia has played a role in many emerging markets portfolios because it provides a means of gaining exposure to rising energy prices.

“In light of the Russia-Ukraine conflict, we’ve been looking at more opportunities in the Middle East, where we believe some countries will likely be the main beneficiaries of further sanctions on Russia and the resulting upward pressure on energy prices,” says McClone.

“Generally, then, we have a cautious view of central and eastern Europe,” says Preyss. “On the flip side are countries that are commodity beneficiaries, many of which are in the Middle East – such as the UAE and Qatar – and Latin America. Banks in Middle Eastern countries may also perform well in the coming years because interest rates there have tended to rise with U.S. rates.”

Latin America also appears to have some other things working in its favor. Countries are reopening after enduring a difficult two years of Covid-related shutdowns, and valuations in some countries (especially in Brazil) are attractive.

The overall outlook for Asia is mixed. “We believe compared to Asia more broadly Southeast Asia is better positioned. Indonesia in particular is responding to positive trends, including a post-Covid reopening and higher commodity prices.”

Preyss also believes some smaller, peripheral Asian countries could see compelling equity market performance this year. “Smaller countries tend to have smaller markets with smaller companies. That broadening of investment opportunities by region and market cap is exciting for us as all-cap investors,” he says.

And what about China? Among the positives, as President Xi begins his third term (likely as the first Chairman since Mao) sometime in the fall. The government is focused on ensuring a stable economic environment preceding that event.

“I suspect we will see moderate fiscal stimulus, and on the monetary side, China will probably be one of the only major central banks to ease in 2022. We are observing some easing of regulatory pressures, and valuations are also very attractive, in our opinion,” says Preyss.

In addition, while Covid has been a drag on China’s economy, we are seeing some relaxation of strict lockdowns in previous months. The official NBS non-manufacturing purchase managers index (PMI) for China dropped to 48.4 in March, marking the first decline in the service sector since last August 2021. However, it later surged to 54.7 in June. The property market is still under significant stress, and consumer sentiment has been weak since the second half of 2021.

“There’s also the heightening geopolitical risks between the U.S. and China, and the rhetoric will likely ramp up as the U.S. mid-term elections near,” says Preyss. “All things considered, I believe we could see a significant weakening of growth in China, so we’re taking a bottom-up view and focusing on identifying companies with strong underlying fundamentals.”

This content is for informational and educational purposes only and not intended as investment advice or a recommendation to buy or sell any security. Investment advice and recommendations can be provided only after careful consideration of an investor’s objectives, guidelines, and restrictions.

Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within William Blair Investment Management, LLC, or affiliates. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented. Investing involves risks, including the possible loss of principal. Investing in foreign securities may involve heightened risk due to currency fluctuations, and economic and political risks. These risks may be enhanced in emerging markets. Past performance is not indicative of future returns.